a wonky take on insurance

I get many emails from a wide variety of public relations people and topics. The one below is an example of something that is not directly in the realm of emergency management and disasters, but it is about insurance and the challenges insurers are facing in trying to figure out the future.

My take from a non-technical point of view:

They need more data to make good decisions

Multiple data sets make it harder to achieve a big picture assessment

They need data integration to see the impacts across information sources

Complexity is something we are all dealing with in our modern environment

Looking at risk exposures and needing more personnel talent in the form of risk management expertise

More consolidation in the industry is expected

There are likely more takeaways, but I’m not smart enough to spot them!

In summary, I don’t think they have a handle on how to price their products and what their true vulnerabilities are.

CWAN Finds Data Integration Gap Creates Competitive Opening as APAC Insurers Eye Private Markets

149 of 150 Executives Cite Data Challenges as Private Market Allocations Surge to 33% and M&A Accelerates

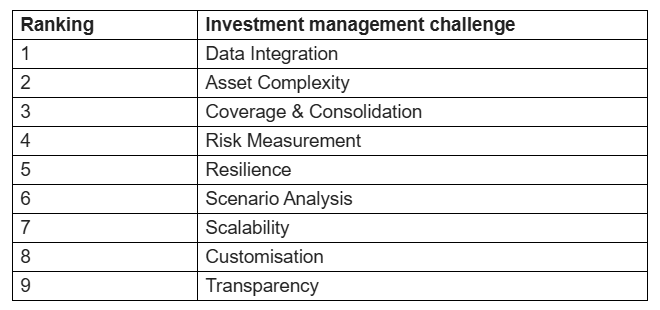

January 28, 2026 – The most pressing challenge facing insurance asset managers is data integration, closely followed by asset complexity, and then coverage and consolidation. While data integration ranks as the top challenge, only 42% rate their systems as excellent at handling it, according to new research* from Clearwater Analytics (NYSE: CWAN), the most comprehensive technology platform for investment management.

The disconnect is even more pronounced for asset complexity, ranking second in importance but dead last in performance, with just 23% confident in their systems’ capabilities.

The study with insurance asset management executives at firms based in Asia Pacific with $3.823 trillion in total assets under management reveals near-unanimous consensus on the data crisis; of 150 executives surveyed, only one disagreed that data coming from external managers in multiple formats makes it harder to access critical information.

When asked about key investment management challenges, Data Integration – managing data from third parties and from multiple internal and external systems – ranked as their top concern. Asset Complexity – structuring and pricing of structured products, exotics, and other complex instruments – ranked second. Coverage and Consolidation – aggregating risk exposures across portfolios, strategies, and trading desks to provide a firm-wide view – ranked third.

These challenges will only intensify, as 88% plan to increase diversification over the next three years, with private market allocations expected to grow from 20% to 33% of holdings within five years. Meanwhile, 66% are increasing their use of third-party asset managers, multiplying data complexity exponentially.

The survey also explored how insurers are responding to skills and capability gaps within investment management functions. The top strategies included recruiting people from a wider range of sectors or with more diverse perspectives; hiring more specialists in risk management roles; adding new tools or platforms to compensate for system deficiencies; increasing training levels; and outsourcing more to third parties.

Notably, more than nine in 10 (92%) respondents agreed (with 35% strongly agreeing) that insurers are now working with more asset managers than they were before, resulting in data arriving in multiple formats and making it more difficult for them to access the information they need.

“As insurers diversify their investment strategies and engage more external managers, the ability to unify, normalise and analyse data across disparate asset classes and systems has become critical,” said Shane Akeroyd, Chief Strategy Officer and President of Asia Pacific at CWAN. “With private markets set to represent a third of future allocations and 72% reporting increased risk profiles, firms can no longer afford the performance gaps we’re seeing in foundational capabilities.”

“These findings reinforce what we see every day from organisations,” added Akeroyd. “There is an operational demand for integrated platforms that simplify complexity, strengthen risk oversight and scale seamlessly as portfolios grow and regulations evolve. With 96% expecting increased M&A activity, the firms that close these capability gaps first will have a significant competitive advantage as the sector consolidates.”